Historical Parallels to Today’s Inflationary Episode

By Chair Cecilia Rouse, Jeffery Zhang, and Ernie Tedeschi

Introduction

Supply chain disruptions are having a substantial impact on current economic conditions. Economy-wide and retail-sector inventory-to-sales ratios have hit record lows; homebuilders are reporting shortages of key materials; and automakers do not have enough semiconductors. Elevated consumer demand is adding fuel to the fire. Travel demand, for example, has returned much more sharply than expected, which is straining airline operations. Similarly, total vehicle sales in April more than doubled from a year prior, which is leading to empty dealer lots. The combination of a spike in consumer demand and a supply chain that is not fully operational has contributed to rising prices.

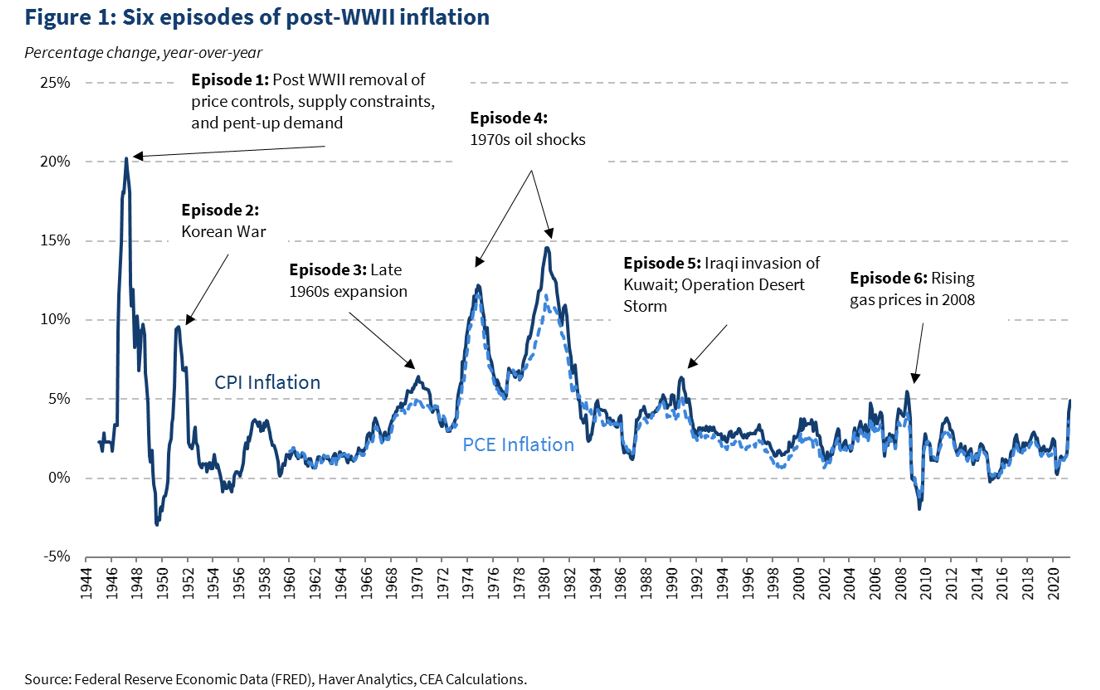

In this blog post, we examine previous periods of heightened inflation and see what they can teach us about inflation in 2021. Figure 1 shows a time series of two commonly used measures of inflation: Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE). Since World War II, there have been six periods in which inflation—as measured by CPI—was 5 percent or higher. This occurred in 1946–48, 1950–51, 1969–71, 1973–82, and 2008. We first present a high-level overview of each of the previous six inflationary episodes and then turn our attention to the years following World War II—an episode that has strong similarities to what is occurring in the current environment.

Six Inflationary Episodes

Episode 1: July 1946–October 1948

Milton Friedman and Anna Jacobson Schwartz (1980) observe that World War II ushered in a period of inflation comparable to the inflationary episodes that occurred during the Civil War and World War I.[1] Prices also surged after World War II ended. In 1947, inflation jumped to over 20 percent, as shown in Figure 1. According to the Bureau of Labor Statistics (BLS), the rapid post-war inflationary episode was caused by the elimination of price controls, supply shortages, and pent-up demand.

Episode 2: December 1950–December 1951

The Korean War started in June 1950 and hostilities ceased in July 1953. Prices had been declining in the months prior to the war because of a mild recession, but rebounded with the return to wartime status. Demand jumped as households—reminded of rationing and supply shortages during World War II—rushed to purchase goods. In addition, some consumer production shifted back to military material, and price controls were reinstated. Notably, in the post-Korean War years, when price controls were removed, inflation did not jump the way it did following World War II.

Episode 3: March 1969–January 1971

This inflationary episode was caused by a booming economy, which increased prices. From 1965 through 1969, for instance, real quarterly GDP growth averaged 4.8 percent at an annual rate. Inflation fell after President Nixon instituted a freeze on wages and prices.

Episode 4: April 1973–October 1982

In the 1970s, the United States experienced its longest stretch of heightened inflation because of two surges in oil prices. The first was caused by an oil embargo implemented by the Organization of Arab Petroleum Exporting Countries (OPEC). The second surge was caused by a decline in oil production due to the Iranian Revolution and the Iran–Iraq War. In 1979, Paul Volcker became the Chair of the Federal Reserve and began his well-known campaign of hiking interest rates to bring inflation under control.

Episode 5: April 1989–May 1991

This fifth inflationary episode occurred when Iraq invaded Kuwait, leading to the first Gulf War. The price of crude oil increased significantly due to heightened uncertainty, leading to a short bout of high inflation.

Episode 6: July 2008–August 2008

In 2008, the CPI rose above 5 percent for two months due to skyrocketing gas prices. One barrel of West Texas Intermediate crude oil cost more than $140 in July 2008 compared to $70 just a year earlier.

Pent-up demand and supply chain disruptions

The three most recent inflationary episodes were largely a function of oil shocks; in contrast, pandemic price dynamics have not been primarily driven by oil supply, though we continue to closely monitor ongoing energy price behavior. In addition, oil prices have a different relationship with the American economy than in the past, as the United States became a net annual petroleum exporter in 2020 and uses an increasing share of renewables for its energy consumption. The episode from 1969–71 is also different because the economy was growing quickly at nearly 5 percent per year for half a decade, which is not the case at present. The episode during the Korean War is a closer comparison, as households rushed to buy goods in anticipation of a supply shortage. While households are consuming more today in the aftermath of COVID due to pent-up demand, they are not hoarding in anticipation of a supply shortage. Also, while many industries face supply constraints, there is not a broad push to shift production away from consumer goods.

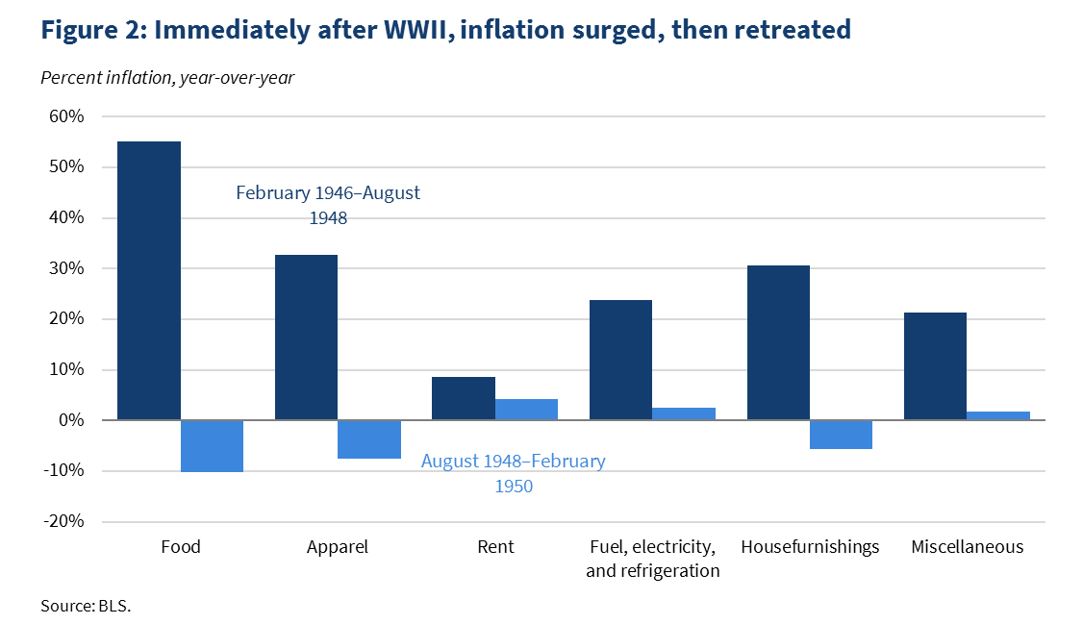

The period right after World War II potentially provides the most relevant case study, as the rapid post-war inflationary episode was caused by the elimination of price controls, supply shortages, and pent-up demand. Figure 2 shows the change in prices in the five years following World War II.

Not surprisingly, supplies were running low or were exhausted entirely during the war. Families had trouble buying cars and household appliances because they were essentially unavailable. According to the BLS, “[by] 1943, many durable goods, such as refrigerators and radios, were also dropped from the [CPI] as their stocks were exhausted.” Instead of focusing on consumer or industrial durable goods, manufacturing capabilities were concentrated on military production. Today’s shortage of durable goods is similar—a national crisis necessitated disrupting normal production processes. Instead of redirecting resources to support a war effort, however, manufacturing capabilities were temporarily shut down or reduced to avoid COVID contagion.

Pent-up demand also put upward pressure on prices following World War II. During the war, households were limited by the widespread rationing of consumer goods. The government rationed foods such as sugar, coffee, meat, and cheese as well as durable goods like automobiles, tires, gasoline, and shoes. Personal savings increased significantly and were spent soon after the war ended. Between 1945 and 1949, a population of roughly 140 million Americans purchased 20 million refrigerators, 21.4 million cars, and 5.5 million stoves. During COVID, businesses were shut down and households mostly stayed indoors. Expenditures on entertainment, dining at restaurants, and travel fell dramatically (from March 20–26, 2020, the entire U.S. box office made roughly $5,000 as compared to $200 million during the same week in 2019). Personal savings increased during the pandemic as well, and now retail sales are booming.

One substantial difference between the inflation dynamics of World War II and today is that price controls were a wartime policy tool that were not implemented during COVID. Those price controls reduced the price level 30 percent below what it would have been otherwise, according to Paul Evans (1982). When the caps were lifted in 1946, prices climbed significantly. For example, food prices alone rose 13.8 percent in July after food price controls expired on June 30th.

According to Benjamin Caplan (1956), the inflationary episode after World War II ended after two years as domestic and foreign supply chains normalized and consumer demand began to level off. (Caplan also observes that private fixed investment started to decline, which contributed to the decline in prices and caused the economy to fall into a mild recession, with real GDP declining by 1.5 percent).

The role of expectations

If actual inflation is affected by inflation expectations—and if expectations are in part formed by recent experiences (what economists call “adaptive” expectations)—then one risk is that transitory supply constraints and pent-up demand could have more persistent effects by raising longer-run expectations of inflation. On the other hand, businesses and consumers may “see through” supply disruptions and not change their longer-run expectations significantly.

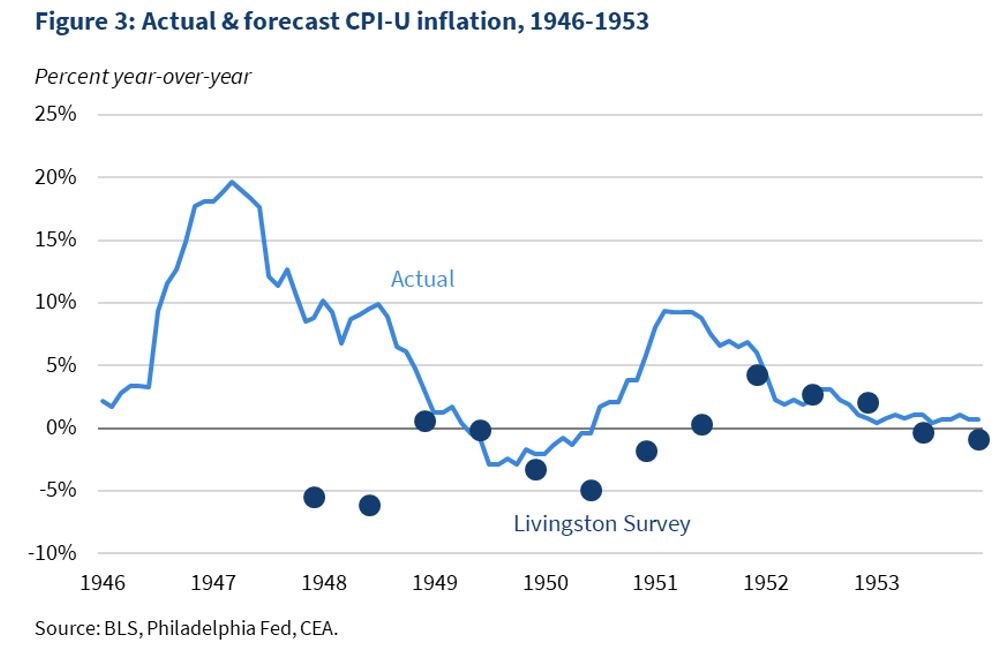

The United States of 1946 did not have nearly as many ways of gauging inflation expectations as we do today, but the limited data we have suggest Americans at the time were aware of the transitory nature of their inflationary episode. The Livingston Survey of economic forecasters—begun in June 1946 by a columnist for the Philadelphia Inquirer and run today by the Federal Reserve Bank of Philadelphia—shows that forecasters expected low or even negative inflation over the 1947–1951 period (see Figure 3 below). While actual inflation often came in higher during this time—and early expectations surveys like Livingston should be interpreted with caution due to difficulties in knowing how respondents were calibrating their expectations—respondents did not appear to persistently mark up their short-run inflation forecasts due to the transitory inflation episodes of World War II and the Korean War.

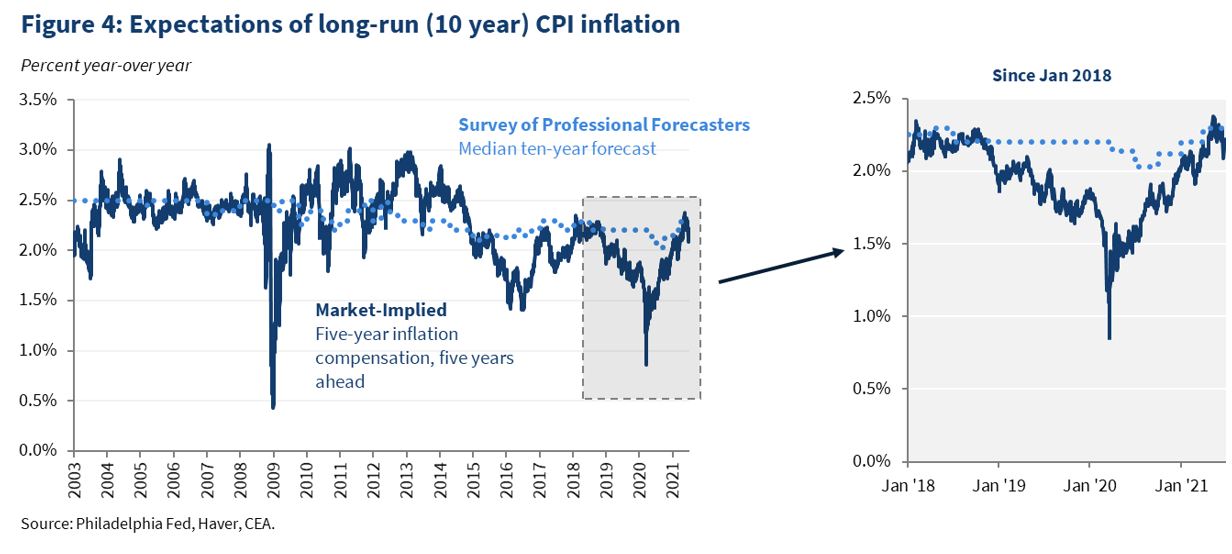

Today, we have metrics measuring longer-run inflation expectations in the form of surveys and market-based measures. If transitory inflation pressures were spilling over into longer-run expectations, we would anticipate seeing these measures rise to historically high levels. However, as Figure 4 below shows, both market-based measures like the five-year, five-year inflation break-evens, and survey-based measures like the ten-year expectations in the Survey of Professional Forecasters, have broadly recovered from pandemic-lows to levels more consistent with pre-pandemic expectations.

Conclusion

No single historical episode is a perfect template for current events. But when looking for historical parallels, it is useful to concentrate on inflationary episodes that contained supply chain disruptions and a spike in consumer demand after a period of temporary suppression. The inflationary period after World War II is likely a better comparison for the current economic situation than the 1970s and suggests that inflation could quickly decline once supply chains are fully online and pent-up demand levels off. The CEA will continue to carefully gauge the trajectory of inflation.

[1] Due to limitations in comparable CPI data, our analysis begins at the end of World War II.