Life After Default

By Chair Cecilia Rouse, Ernie Tedeschi, Martha Gimbel, and Bradley Clark

The credit of the United States is built on centuries of stability and responsibility. This country has never intentionally defaulted on its obligations because of the debt limit. But the U.S. Treasury Department estimates that it will have very limited resources to avoid doing exactly that for the first time unless Congress raises or suspends the debt ceiling by October 18th. If Congress fails to act, it could take decades for the United States to fully recover.

A default would fundamentally hinder the Federal government from serving the American people. Payments from the Federal government that families rely on to make ends meet would be endangered. The basic functions of the Federal government—including maintaining national defense, national parks, and countless others—would be at risk. The public health system, which has enabled this country to react to a global pandemic, would be unable to adequately function.

Furthermore, a default would have serious and protracted financial and economic effects. Financial markets would lose faith in the United States, the dollar would weaken, and stocks would fall. The U.S. credit rating would almost certainly be downgraded, and interest rates would broadly rise for many consumer loans, making products like auto loans and mortgages more expensive for families who are subject to interest rate changes or taking out new loans. These and other consequences could trigger a recession and a credit market freeze that could hurt the ability of American companies to operate.

In an accompanying blog post, we explain what the debt limit is. In this post, we go further, and lay out the risks that Americans and the U.S.—and global—economy will face in the days, months, and years after a default.

The Federal government would be immediately impaired from carrying out its basic functions, including providing the financial assistance that tens of millions of Americans rely on.

Everyone in America would feel the effects of a default. If the United States were to default, tens of millions—including families with children, retirees, and veterans—would quickly, even overnight in some cases, face the prospect of losing the regular Federal payments that help them to make ends meet.

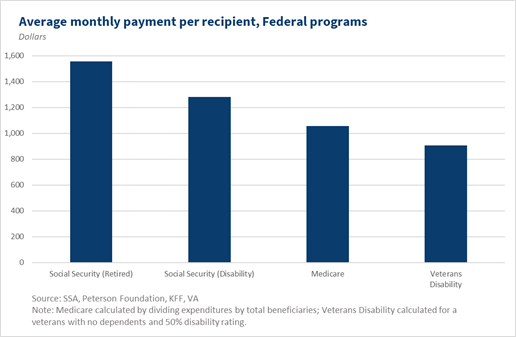

In 2020, almost 50 million residents received retirement benefits through Social Security, and 6 million received survivors benefits. In 2015, around 12 million people relied on Social Security as their sole means of support.[1] As shown in Figure 1, the average retired Social Security recipient counts on receiving almost $1,600 per month. Among households receiving any Social Security benefits, those benefits make up more than half of household income on average.[2] And yet, if we default, these Americans may not receive their Social Security payments on time, or even at all.

Health coverage during a pandemic would also be in doubt. Over 60 million people across America are on Medicare, 75 million are enrolled in Medicaid, and almost 7 million children receive coverage through the Children’s Health Insurance Program (CHIP). Net Medicare payments, alone, amount to about $1,100 per recipient. Although affordable health care is vital, particularly during a pandemic, millions could find themselves without coverage.

A default threatens veterans’ programs as well, with over 9 million veterans relying on physical and mental care, in addition to other supports. For a single veteran with a 50 percent disability rating and no dependents, the average disability benefit is around $900 per month; veterans with families or with greater disability ratings receive more.

If the Federal government ended up missing or delaying payments, millions would be unable to put food on the table or pay rent. Before the full weight of the Federal pandemic response had come to bear, the hardships experienced early on—exemplified by families going hungry and waiting in food lines—remind us of the raw misery that inadequate Federal support brings in the wake of an economic shock.

Examples of other important forms of Federal assistance that would also be at risk are outlined in the table below. This is an underrepresentation, of course, as the Federal government is responsible for funding many programs on which Americans rely—from childcare, to cash assistance, to aid for small business owners.

| Table 1. Number of participants by government program | |

| Program | Number of Participants |

| Supplemental Nutrition Assistance Program (SNAP) | 42 million people |

| Child Tax Credit (CTC) | 60 million children |

| Housing Assistance | 10 million people |

| Financial Aid | 11 million students[1] |

| School Lunch Program | 30 million children |

Moreover, many benefit from different Federal programs at once. Consider the impact of the Federal government not fulfilling its obligations on three illustrative American families: an elderly couple, a veteran living alone, and a young family with two children. All of them benefit from the Federal government in a myriad of ways. For instance, as seen below, a typical married elderly couple relies on more than $4,800 a month just from Social Security and Medicare, not to mention other programs they qualify for.

- A married elderly couple aged 70.

- Social Security: $3,197/month

- Medicare: $1,635/month

- A disabled veteran, receiving special monthly compensation finishing college at age 35.

- Veterans’ disability benefits: $1,428/month

- Education aid: $1,740/month

- A young married couple making $40,000 with two children, 4 and 6.

- Child Tax Credit: $600/month

- Low-Income Home Energy Assistance Program: $440/month

- Special Supplemental Nutrition Program for Women, Infants, and Children: $40/month

The Federal government’s ability to provide for the national defense, pandemic response, and day-to-day services would likely be severely hampered.

There are many other functions of the Federal government that we often take for granted and that would be in peril after a default. For example, the Federal government keeps our country safe by paying the salaries of 1.4 million active duty military personnel and their families. The deployment of personnel, the maintenance of equipment, the procurement of supplies, and other support activities would risk being frozen after a default, hampering the defense of the country at a time when there are ample threats to national security. The same holds for expenses related to counter-terrorism and intelligence measures, which could leave America more vulnerable to potential threats.

The Federal health response to COVID requires inspections and certification of medications that could halt without funding, including vaccine and therapeutic approvals through the FDA, just as the COVID vaccine for American children is going through the approval process. Other critical day-to-day services would also be under threat, including the operation of our national parks, mail delivery, consular services in other countries (which support American residents abroad), and air traffic control—which could potentially ground passenger and cargo planes.

There are also services that, many Americans probably do not realize, depend on Federal support. For instance, in the event of a default, the National Weather Service might struggle to deliver important weather information to families, local news stations, and businesses. The ability to listen to and communicate via radio would be at risk, as the radio telecommunication system is organized by the Federal Communications Commission. Even the official time of the United States is maintained by the National Institute of Standards and Technology, which is crucial to computing and travel, since GPS devices are reliant upon accurate official clocks.

The effects of a default go far beyond the lack of financial assistance to those in need. Everyday services crucial to a functioning society—many of which seemingly run in the background of our lives—would be at risk. An inability to pay for these services would cause large disruptions for the entire country.

Markets and consumers would be hurt by even the threat of a default, much less an actual default.

Finally, a default—or even just the threat of one—would have a devastating impact on our economy. In the run-up to and aftermath of the 2011 debt ceiling crisis—where the country ultimately avoided a default—market risk measures rose persistently, and measures of consumer confidence and small business optimism weakened. Mortgage rates rose by between 0.7 and 0.8 percentage point for two months after that year’s debt ceiling crisis passed, and only declined slowly thereafter.[4] For a family taking out a $250,000 30-year fixed-rate mortgage, an extra 0.8 percentage point means more than $30,000 in additional interest payments over the life of the loan. Rates for auto loans, personal loans, and other consumer financial products also rose in the wake of the 2011 crisis,[5] and these increases often lasted for months. This all happened despite the fact that Congress acted to avoid default in time, before the U.S. Treasury exhausted its cash on hand and its other means of financing.

While past experiences can help us put a floor on what to expect if the Federal government failed to meet its obligations, they likely underestimate the effects of what the United States would face. An actual default—even if resolved quickly—would very likely have even more pronounced effects and deeper financial scarring.

The consequences of a default could accelerate rapidly if not resolved, potentially inducing a global financial crisis and a recession.

If the United States does default, the consequences could escalate rapidly and profoundly. The timeframe of these impacts is unclear, since the United States has never defaulted; moreover, the effects of a default would not be confined to the United States. The global economy, which relies on a strong U.S. economy, would begin to slide into a financial crisis and likely, a recession. U.S. Treasury debt is the world’s benchmark safe asset, and its interest rates act as the basis for the pricing of countless financial products and transactions around the globe. The U.S. dollar is also the world’s premier reserve currency. A default would send shock waves through global financial markets and would likely cause credit markets worldwide to freeze up and stock markets to plunge. Employers around the world would likely have to begin laying off workers. The 2008 financial crisis had ripple effects throughout the global economy that ricocheted back to U.S. shores, causing firms to lay off workers and cut private investment.[6] A financial crisis driven by a default has the potential to be even worse, in addition to hitting a global economy not fully recovered from the pandemic.

In the United States specifically, past simulations by the Federal Reserve[7] and the Peterson Foundation[8] that look at the possible month-long default in 2013 suggested that unemployment would increase and remain elevated for at least two to four years afterwards. Projections in a recent report released by Moody’s are even more dire, suggesting that under a prolonged 4-month default, real GDP would fall by 4 percent, unemployment would rise to almost 9 percent, and the U.S. economy would lose nearly 6 million jobs. For context, during the two years of the Great Recession, real GDP fell by 4.3 percent, unemployment rose to 10 percent, and the economy lost almost 9 million jobs.

Compounding the damage of a default is the fact that the Federal government would be immobilized in responding to the very economic crisis a default would likely create. It would likely not be able to implement relief of the type that proved so vital to helping families during past economic crises, and more recently, during the coronavirus pandemic. Instead, the Federal government could only stand back, helpless to address the economic maelstrom.

Conclusion

In short, the United States has never intentionally defaulted on its obligations for one reason above all others: the self-inflicted economic ruin of doing so would be catastrophic. Just the threat of a default has negative effects on the U.S. economy, and an actual default for any amount of time would inflict a devastating blow that would be felt by families, businesses, and the economy here and globally for decades to come. The debt ceiling is not and should not be used as a political football. The consequences are too great.

A previous version of this blog post mentioned that maintenance of the power grid through the Federal Energy Regulatory Commission (FERC) would be under threat in the event of a default. While FERC does have a role in implementing reliability standards for the bulk power system, the Commission does not have a role in operating the grid itself.

[1] Using numbers from CBPP, the 12 million people who relied solely on Social Security in 2015 specifically relied on old age and survivors insurance.

[2] Based on CEA analysis of the 2021 CPS ASEC, this applies to 54 percent of households that receive Social Security benefits.

[3] Data from 2015-2016.

[4] Source: Haver Analytics, Wall Street Journal, and Federal Reserve Board

[5] Source: Haver Analytics, Wall Street Journal, RateWatch, and Federal Reserve Board

[6] For instance, many firms rely on short-term loans to make everyday payments, such as payroll. If credit markets freeze or loans become too expensive, firms may struggle to pay employees.

[7] Engen, Eric, Glenn Follette, and Jean-Philippe Laforte. (2013). “Possible Macroeconomic Effects of a Temporary Federal Debt Default. Report Authorized for Public Release by Federal Open Market Committee. [link]

[8] Macroeconomic Advisers, LLC. (2013). “The Cost of Crisis-Driven Fiscal Policy.” Report Prepared for the Peterson Foundation. [link]