The Biden Economic Agenda, Two Years In

By Brian Deese, Director of the National Economic Council

Just over two years ago, then-President-elect Biden addressed the nation in a prime time speech to propose his economic agenda: a plan for a strong, worker-centered economic recovery from the pandemic, followed by long-term investments to lay the foundation for more durable, resilient, and inclusive long-run growth.

In those remarks, the President made a series of concrete commitments to the American people about his plan for economic recovery and renewal. This blog post reviews those commitments and progress made in the two years since they were made.

The President refers to his economic strategy as bottom-up and middle-out economics. That strategy starts with the idea that we should prioritize economic policies that help workers and families recover from economic downturns, avoid the scarring that is too often associated with joblessness and other economic challenges, and provide lower-income and middle-class Americans more breathing room by lowering the costs they face.

Building from the bottom up and middle out also means investing in America – in infrastructure, innovation, and clean energy – in ways that rebuild our industrial strength and supply chains, and expand the productive capacity of the economy. This includes making historic, capacity enhancing investments in our physical infrastructure and our people. It means catalyzing and crowding in private investment in high-growth and high-potential industries, including those that are central to our national security, economic security, and climate and clean energy goals. These kinds of investments won’t just enhance productivity and grow the economy over time – but they can also facilitate more inclusive economic growth that improves living standards for workers and boosts a host of economic outcomes in communities that have long suffered from disinvestment.

Two years in, a review of these commitments underscores that President Biden’s economic strategy is working. Economies around the world including the United States have struggled with pandemic-driven price increases. But we have made important progress in bringing inflation down while maintaining a resilient recovery. In fact, the United States is better-positioned than other major economies to navigate the transition to steady, stable growth with lower inflation and without giving up all the economic gains we have achieved over the last two years. While there is more work to do, and we may face setbacks along the way, the policy strategy we have executed positions us uniquely well to come out of the pandemic crisis stronger, more resilient, and prosperous for years and decades to come.

Take bold action to get American workers back into jobs

“Some 18 million Americans are still relying on unemployment insurance…And it’s not hard to see that we’re in the middle of the once in several generations economic crisis with a once in several generations public health crisis. The crisis of deep human suffering is in plain sight and there’s no time to waste. We have to act and we have to act now.”

The President-elect began his speech on January 14, 2021 by emphasizing the urgency of bold action to get American workers back into jobs.

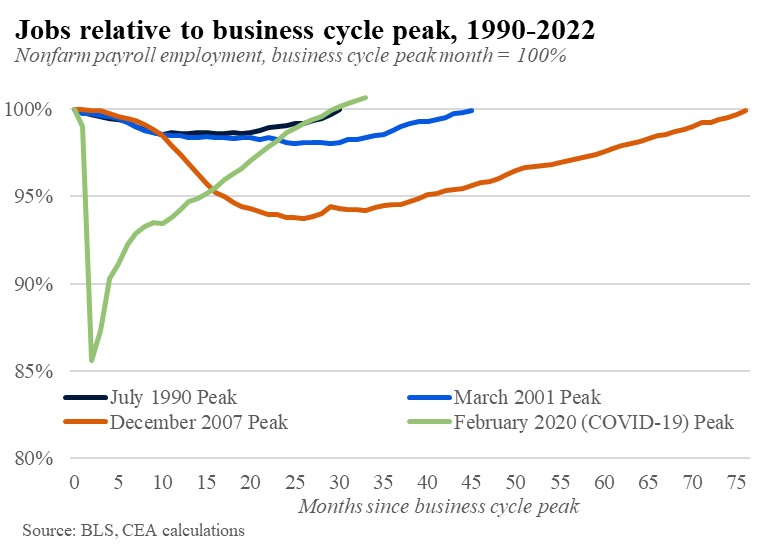

Since then, the economy has recovered all of the jobs lost during the pandemic downturn and it did so faster than in the aftermath of the last three major economic downturns – the 1990 – 1991 and 2001 recessions, and the 2007 – 2009 Great Recession.

2021 and 2022 – President Biden’s first two years in office – were the strongest years of job creation on record. Similarly, the share of prime working age Americans in jobs or looking for work is higher now than it was in almost the entire decade before the pandemic began – and has recovered more of the lost ground than at this time in the last two downturns.

Moreover, the unemployment rate fell to a 50-year low at the end of 2022, with the unemployment rate near record lows for African-Americans and Hispanics and at the lowest rate in history for people with disabilities. In the context of this uniquely strong labor market, wages have gone up the most for lower- and middle income workers.

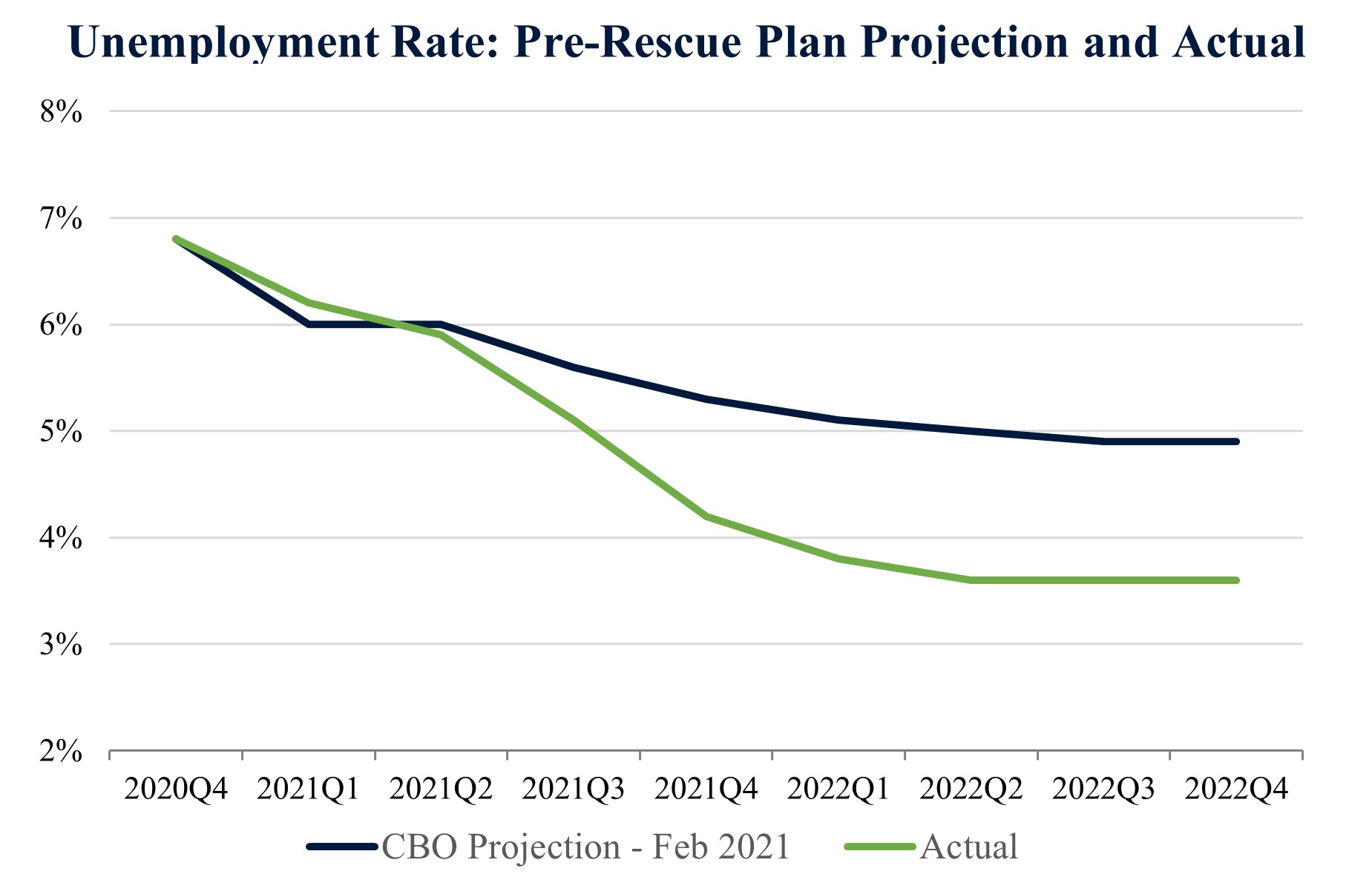

This progress was far from pre-ordained – it was driven by decisive policy action to get Americans back to work. Before the passage of the American Rescue Plan, the nonpartisan Congressional Budget Office projected that the unemployment rate would be 4.9% in the final quarter of 2022, rather than the 3.5% it actually reached.

The policy priority on driving a strong labor market recovery was grounded in decades of economic research showing that long spells of unemployment have severe and long-lasting “scarring” impacts on workers, families, and communities: long-term unemployment makes it harder to find future jobs or acquire new skills; it drives higher rates of depression and substance abuse; it puts financial distress on families; and it has devastating educational and economic effects on children. It is particularly noteworthy, in this context, that long term unemployment is down by more than 3 million people from its March 2021 peak, and is currently well below its 2010-2019 average.

Throughout this period, the Administration has also taken direct action – through the National Labor Relations Board and the President’s Task Force on Union Organizing and Worker Empowerment – to promote the strength of unions. In part as a result, petitions for union representation elections were up 53% in the private sector in 2022.

Accelerate the Federal Government’s response to end the COVID-19 pandemic

“Our rescue plan starts aggressively in order to speed up our national COVID-19 response.”

The President identified early on that economic recovery was inextricably tied to ending the COVID-19 pandemic’s grip on our economy and our lives. To safely put Americans back to work, we had to rapidly develop and deploy vaccines, increase testing access, and reopen our schools and businesses. He also recognized that pandemic conditions were highly uncertain, and we needed to prepare for risks were at the time unknown but ultimately materialized, like the Delta and Omicron variants.

Two years later, COVID deaths are down over 80%. Vaccines, treatments like Paxlovid, and testing are ubiquitously available; and our schools and businesses are open again. We are far better positioned to deal with surges and new variants than before.

All the while, the President has worked to limit the potential economic disruptions from the pandemic – shortages of essential products like medicine and food, shortages of personal protective equipment (PPE) for front-line healthcare workers and the general public, and shortages and disruptions that arose across the economy due to global pandemic-oriented supply chain challenges.

The Administration, for example, brought business and labor together to broker an agreement to move ports to 24/7 operations, which has helped increase goods movement through the Ports of Los Angeles and Long Beach by 24% above pre-pandemic record levels, while bringing goods transportation prices down. The Administration launched a Trucking Action Plan to increase the supply of truck drivers in good jobs, which helped to double the number of new commercial driver’s licenses issued. The Administration also worked with Congress to pass the bipartisan Ocean Shipping Reform Act, lowering costs for consumers. As of December, a leading index of supply chain pressures showed that more than 70% of pandemic-oriented supply chain pressures had eased.

Help American households avoid the worst economic outcomes associated with downturns

“Our rescue plan also includes immediate relief to Americans, hardest hit, and most in need… It will also provide more peace of mind for struggling families… And as we work to keep people from going hungry, we’ll also work to keep a roof over their heads, to stem the growing housing crisis and evictions that are looming.”

Part of the logic behind bold action to spur a rapid labor market recovery and provide relief to households was the necessity of helping households avoid some of the most negative economic outcomes that are often associated with downturns – things like evictions and foreclosures, bankruptcies, and loss of health care coverage.

As shown below, financial security for households on a range of measures is not only better than it was during the depths of the pandemic, but, critically, measures of financial security have also generally improved compared to both pre-pandemic levels and averages from 2010-20191. Because of policies President Biden has signed into law, we have reduced health care costs and expanded access – leading to the lowest uninsured rate on record in 2022. In other words, because of focused and decisive policy action, households are coming out of the pandemic better off than before on key metrics of economic security – something that typically takes years to happen after economic downturns. And while inflation has undoubtedly posed challenges to economic security, wages increased faster than inflation in the second half of 2022 – as gas prices declined substantially, core inflation moderated, and the labor market remained strong – providing further tangible economic benefit to workers and families.

| Indicator | Change from Pre-Pandemic | Change from 2010-19 Avg |

| Credit card delinquency rate | -21% | -26% |

| Mortgage delinquency rate | -20% | -72% |

| New delinquent auto loan balances (% of current balance) | -10% | -14% |

| Overall delinquency rate, 30+ days | -16% | -65% |

| Number of new bankruptcies | -51% | -67% |

| Evictions | -30% | NA |

| Share that can afford a $400 cash expense | 8% | 20% |

| Uninsured Rate | -19% | -30% |

| *Q3 for all indicators except share of individuals that can afford $400 cash expense (2021), evictions (Dec. 2022), and uninsured rate (first half of 2022). ** 2010-2019 average except for share of individuals that can afford a $400 cash expense (2013-2019). Source: Federal Reserve Board, Federal Reserve Bank of New York, Eviction Lab (city level) National Center for Health Statistics. |

Give small business the support they need and spur renewed entrepreneurship

“Our rescue plan will also help small businesses that are the engines of our economic growth, our economy as a whole, the glue that holds communities together as well.”

The President knows that small businesses are engines of economic growth and employment in communities throughout the country. Over the last two years, the Biden-Harris Administration has provided billions of dollars in pandemic relief, investment, lending, and technical assistance to level the playing field and allow small businesses to thrive.

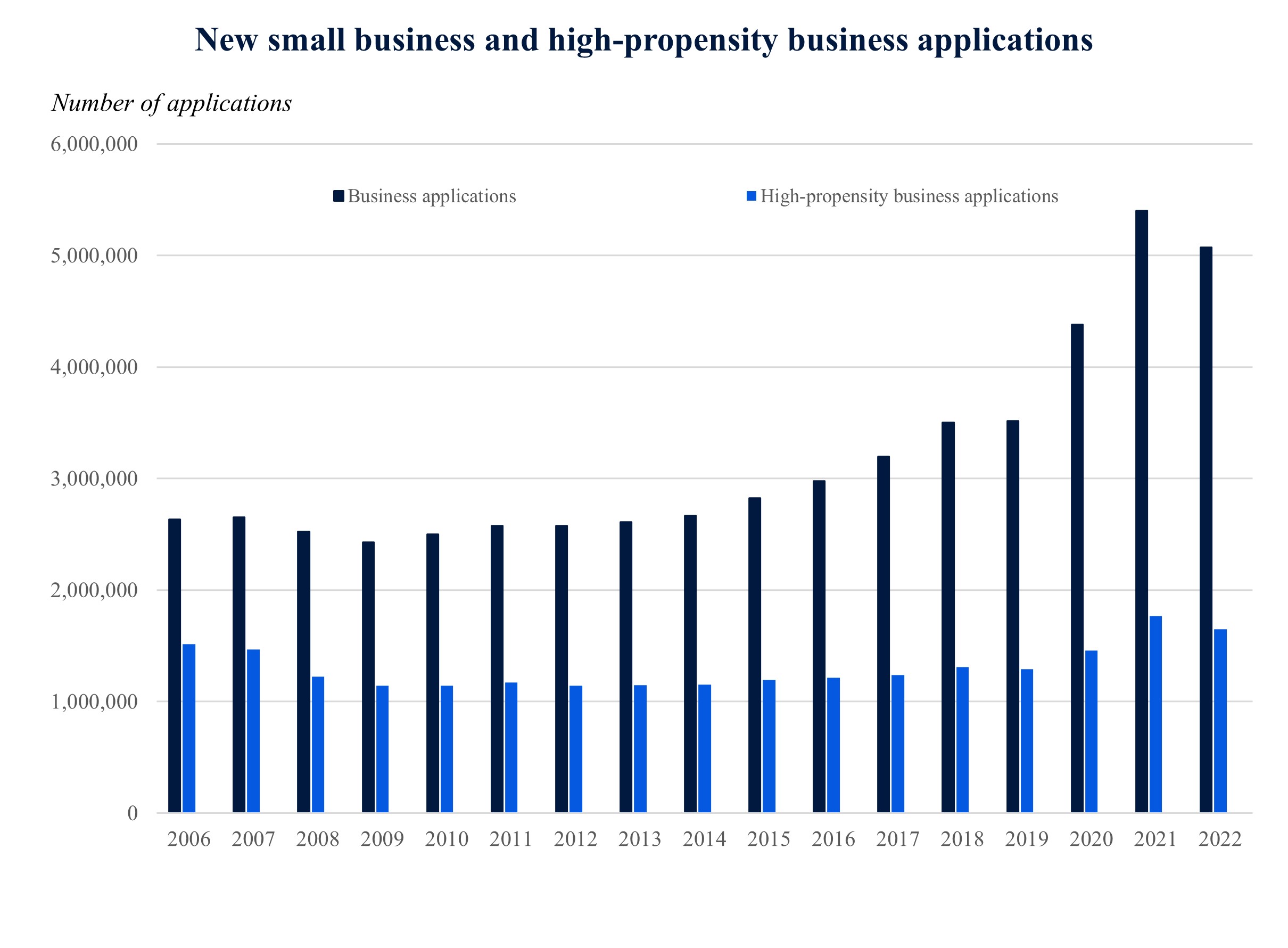

Beyond helping small businesses stay afloat, the Biden economic agenda has also helped drive an unprecedented surge in entrepreneurship. Just this week, new data show that over the last two years, Americans have applied to start 10.5 million new businesses, the strongest two years on record. In 2022, Americans applied to start 5 million new businesses, the second most on record only behind the 5.4 million applicants filed in 2021.

Each of these new small businesses is an act of optimism – people everywhere in the country are putting their own money and their own lives into something new, and they’re doing it in record numbers.

Jumpstart the economy while avoiding the long-term damage to debt and deficits

“It’s not just that smart fiscal investments, including deficit spending, are more urgent than ever, it’s that the return on these investments in jobs, racial equity, will prevent long-term economic damage and the benefits will far surpass the cost.”

The President-elect noted in his speech that the Rescue Plan he proposed wouldn’t just be good for our economy and workers, but it was also the smart thing to do from a fiscal standpoint: that by passing the Rescue Plan, we could jumpstart the economy and avoid the long-term damage to debt and deficits that are associated with slow recoveries, low tax receipts, and prolonged emergency spending.

In the last two years, in addition to the substantial economic benefits stemming from the historically strong recovery, we have also seen significant deficit reduction – as the Rescue Plan facilitated a strong economic recovery and enabled the responsible wind-down of emergency spending programs. Building on this fiscal progress, the President last year signed into law the Inflation Reduction Act, which makes historic progress on reducing energy and health care costs while reducing the deficit by more than $200 billion over the next decade.

Make long-overdue investments in America’s infrastructure

“It’s time to stop talking about infrastructure and to finally start building an infrastructure so we can be more competitive. Millions of good paying jobs that put Americans to work, rebuilding our roads, our bridges, our ports, to make them more climate resilient, to make them faster, cheaper, cleaner to transport American made goods across our country and around the world. That’s how we compete.”

While policymakers for decades have called for investment to revitalize American infrastructure, President Biden worked to bring together Democrats and Republicans to pass the largest investment in infrastructure since we built the interstate highway system. Already, the Biden Administration has launched $185 billion in infrastructure projects, including funding for 6,900 projects, reaching over 4,000 communities across all 50 states, D.C., and the territories. From our roads and bridges to rail, public transit, and the first nationwide network of electrical vehicle chargers to universal high-speed internet, the Biden economic agenda is enabling the kinds of infrastructure investments that economists have long argued would boost economic capacity and crowd-in private investment.

Support for the future of clean energy, manufacturing, and innovation

“American manufacturing was the arsenal of democracy in World War II. It will be so again. Imagine a future made in America, all made in America and all by Americans. We’ll use taxpayers’ dollars to rebuild America. We’ll buy American products, supporting millions of American manufacturing jobs, enhancing our competitive strength in an increasingly competitive world.”

“Imagine historic investments in research and development to sharpen America’s innovative edge in markets where global leadership is up for grabs, markets like the battery technology, artificial intelligence, biotechnology, clean energy. Imagine confronting the climate crisis with American jobs and ingenuity leading the world.”

Building on the strongest two years of manufacturing job growth in 40 years, the President signed the most significant investment in manufacturing, science, innovation, and industrial strategy in over 50 years. And he then signed the largest public investment in the clean energy transition in U.S. history.

Already, private companies have invested nearly $300 billion in locating manufacturing in the United States – from the Rust Belt to the Southwest – ranging from semiconductors to lithium batteries to clean energy production to electric vehicle manufacturing. Many companies have cited incentives and investments signed into law by President Biden as key reasons for their investments. And critically, many of these investments are in communities that have experienced disinvestment in recent years or are geared towards workers without college degrees – whose labor force participation has mostly declined over the last two decades. In other words, these investments can help our economy thrive over the long-run by raising economic potential, promoting resilience, and limiting future harms associated with climate change.

Reform the tax code so the wealthy and large corporation pay their fair share

“As I said on the campaign trail, we will pay for [these investments] by making sure that everyone pays their fair share, not [by] punishing anybody… It’s the right thing for our economy. It’s the fair thing. It’s the decent thing to do.”

As President Biden came into office, he highlighted the need to reform the tax system so that high-income people and corporations pay their fair share. The 2017 tax law only made an unfair tax system worse, and decades of underfunding for tax enforcement meant that the wealthy and large corporations were able to evade their taxes, even as middle-class workers paid the taxes they owed.

Since then, President Biden has signed multiple revenue enhancing tax provisions that will allow us to raise hundreds of billions of dollars to fund critical national priorities that promote economic growth, while making our tax system more equitable.

One is an investment that will allow the U.S. government to crack down on wealthy tax cheats and improve taxpayer services. Working people pay 99% of the taxes they owe, while the top 1%hides about 20% of their income from tax, including by funneling it through offshore accounts in tax havens that don’t report earnings. The investment President Biden signed into law will reduce the deficit by more than $100 billion by cracking down on wealthy tax cheats. None of the resources will be used to increase audit rates relative to historical levels for small businesses or households with incomes below $400,000; in fact, middle-class taxpayers will see more timely refunds and other service improvements because of these resources.

Another is a 15 percent minimum tax on the corporate profits that large corporations—those with over $1 billion in profits—report to shareholders. This new corporate minimum tax increases taxes only on the large companies that are reporting high profits but paying little to no tax, leveling the playing field for companies that are already paying their fair share.

In addition to these legislative accomplishments, the Administration has made substantial strides in working towards a global minimum tax on corporations. The Administration’s leadership has been critical in working to end the global race to the bottom on corporate taxation, which places a higher tax burden on workers and deprives governments around the world – including the United States – of the ability to raise sufficient tax revenue to invest in economic growth.

When President-elect Biden addressed the nation two years ago, he said he believed that if Congress passed his agenda, we would “come out better off than when we went into the crisis.” Two years later, we can now say that we have done so.

The President’s economic plan has laid the foundation for a bottom-up and middle-out recovery – one of the strongest and most equitable economic recoveries in history. This historic recovery – and legislation the President has signed to address longstanding affordability challenges – has set the stage for a transition to steady, stable growth, with lower inflation, even as we keep our job market resilient. Going forward, we need to build on this progress – by lowering the cost of care to help more parents work; by investing in education and skills training, particularly for those without a college degree; and by investing in children and lowering child poverty in America.

Of course, we face a range of economic risks – from geopolitical uncertainty to the potential for reckless extremism around the full faith and credit of the United States. But two years in, because of the resilience of the American people and the economic policies we have pursued, we are better positioned than we have been in decades to achieve durable, resilient, and inclusive long-run growth that we too often failed to achieve before the crisis.

[1] These data account for the effect of the pause on student loan payments and interest accrual for roughly 45 million federal student loan borrowers that was in place in the prior Administration and that has been extended multiple times by the Biden Administration. Recent research suggests that restarting student loan payments without providing the targeted debt relief the Biden Administration announced last Summer would lead to a spike in default and delinquency rates on student loans above pre-pandemic levels for those borrowers.