Pandemic Prices: Assessing Inflation in the Months and Years Ahead

By Jared Bernstein and Ernie Tedeschi

The COVID-19 pandemic has caused an unconventional recession, and we do not expect the recovery will be typical either. While the paramount policy goals are to control the virus, get to full employment, and make the necessary investments for a more resilient and inclusive recovery, economic uncertainties and risks demand careful attention going forward. One risk the Administration is monitoring closely is inflation.

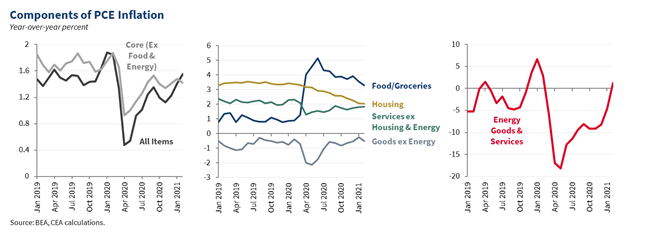

Inflation—or the rate of change in prices over time—is not a simple phenomenon to measure or interpret. Inflation that is persistently too high can hurt the wellbeing of households, especially when it is not offset by comparable increases in wages, leading to reduced buying power. But inflation that is persistently too low leaves monetary policy with less scope to support the economy and can be a sign the economy is below its capacity, thus with room to expand jobs further. Indeed, one piece of important context around the current inflation risks is that inflation was generally weaker than the Federal Reserve’s target over the decade prior to the pandemic as the economy recovered from the Great Recession. Overall inflation, as defined by the Personal Consumption Expenditure (PCE) deflator, then fell further during the pandemic, though there have been important differences between products and sectors (see figures below).

Pandemics of the magnitude of COVID-19 are, thankfully, rare, but that also means few historical parallels exist to inform policymakers. The United States experienced short bursts of inflation in some prior periods of pandemics or large-scale reallocations of economic resources, such as in 1918—driven by the Spanish Flu and demobilization from World War I—as well as the demobilization from World War II after 1945 and the resurgence in defense spending due to the Korean War. But history is not a perfect guide here. The 1957 pandemic, for example, which coincided with a nine-month recession, saw inflation weaken, with no large resurgence even when the pandemic was over and the economy was growing again.

That said, in the next several months we expect measured inflation to increase somewhat, primarily due to three different temporary factors: base effects, supply chain disruptions, and pent-up demand, especially for services. We expect these three factors will likely be transitory, and that their impact should fade over time as the economy recovers from the pandemic. After that, the longer-term trajectory of inflation is in large part a function of inflationary expectations. Here, too, we see some increase, but from historically low to more normal levels. We explain our reasoning below.

Base Effects

In the near-term, we and other analysts expect to see “base-effects” in annual inflation measures. Such effects occur when the base, or initial month, of a growth rate is unusually low or high. Between February and April 2020, when the pandemic was taking hold in the economy, the level of average prices—as measured by the core PCE deflator—fell 0.5 percent, before beginning to rise again in May (core PCE inflation leaves out volatile food and energy prices and thus provides a clearer signal of inflation; however, the same base effects are expected to occur in most price series). This unusually large price decrease early in the pandemic made April 2020 a low base.

Twelve months later, due to the suddenness and scale of this earlier decline, we expect year-over-year inflation growth rates for the next few months to be temporarily distorted by these sorts of base effects. While we do not yet have price data for March or April, if we assume monthly inflation going forward stays at a rate of just under 0.2 percent—the equivalent of a 2 percent annual rate, in line with the Federal Reserve’s target—inflation in April and May 2021, measured as the percentage change in core PCE prices over the previous year, would reach 2.3 percent due to this base effect. Not only is that rate higher than recent inflation growth rates, it would represent a sharp acceleration over current core price growth rates, such as 1.4 percent in February of this year. This broad pattern will be present across different price measures this spring, including the Consumer Price Index (CPI) and Producer Price Index.

The issue with base effects is not that they make inflation measures wrong; the 2.3 percent year-over-year inflation calculation in our illustrative example would still be correct. Rather, the base effects distort our understanding of how underlying, near-term trend inflation is behaving right now, suggesting, for example, higher rates of inflation than most analysts expect to persist. Over the next few months, as the base effects’ months drift further into the past, this distortionary characteristic of the price data should fade.

Supply Chain Disruptions & Misalignments

A second potential source of inflation stems from increases in the cost of production. If the cost of the materials needed to produce a good or service rises (think of the lumber needed to build a house or the electricity needed to power a factory), a business may pass on these costs to consumers in the form of higher prices; economists call this cost push inflation. In most cases, this type of inflation is transitory: the price of lumber or energy rises, but then stabilizes at a higher level or decreases, with no further impact on future inflation. This example underscores an important distinction between price levels and inflation, with the latter being the rate at which levels move up and down.

We have already seen some supply chain disruptions due to the pandemic. For example, the production of parts for goods like automobiles has been curtailed at times, especially in factories in Asia that play an increasingly central role in the global supply chain. Transportation and warehousing costs—ground, air, and ocean—have also risen as cargo logistics have become more difficult. The recent backlog in the Suez Canal will add to these issues in the near term. And surges in demand for certain products, like those that use computer chips, have caused unanticipated supply constraints in industries such as semiconductors.

While we expect global supply chains to gradually unclog as world economies recover throughout 2021 and beyond, in the near-term some businesses may temporarily pass on the added costs from these disruptions into higher consumer prices.

Pent-Up Demand, Especially for Services

Finally, prices for many of the services most sensitive to the pandemic— such as hotels, sit-down restaurants, and air travel—have decreased due to curtailed demand stemming from consumer anxiety and public health restrictions.

As more people get vaccinated throughout the year, however, demand for these and other high-touch services could surge and temporarily outstrip supply. This surge in demand may in part be fueled by savings many households accumulated during the pandemic, as well as relief payments from the fiscal responses last year and this year. For example, Americans may have a high demand to eat out in full-service restaurants again later this year, but may find that there are fewer dining options than were open pre-pandemic. That could prompt restaurants that are still open to raise their prices. And while there are natural limits to how many services we can consume quickly—it’s generally only possible for a family to take one vacation at time, for example—Americans may still try to consume these services more frequently, or may upgrade to higher-quality versions. Economists call inflation resulting from such surges in spending demand pull inflation.

Again, we expect this to primarily be a short-term issue; as businesses that shuttered or substantially reduced their services reopen, supply will increase to meet this pent-up demand. Encouragingly on this point, new business formation has picked up in recent months.

Longer-Term Inflation and Expectations

Over the longer-term, a key determinant of lasting price pressures is inflation expectations. When businesses, for example, expect long-run prices to stay around the Federal Reserve’s 2 percent inflation target, they may be less likely to adjust prices and wages due to the types of temporary factors discussed earlier. If, however, inflationary expectations become untethered from that target, prices may rise in a more lasting manner. This sort of inflationary, or “overheating,” spiral might then lead the central bank to raise interest rates quickly which then significantly slows the economy and increases unemployment. Economists refer to this scenario as “a hard landing,” so inflationary pressures are risks that must be carefully monitored.

It is equally important to recognize that economic “heat” does not necessarily equate with overheating. We expect that moving from a shutdown economy to a post-pandemic economy—with demand fueled by pent-up savings, relief funds, and low interest rates—will generate not just somewhat faster actual inflation but higher inflationary expectations too. An increase in inflation expectations from an abnormally low level is a welcome development. But inflation expectations must be carefully monitored to distinguish between the hotter but sustainable scenario versus true overheating.

The best way to do so is to track various metrics of inflation expectations. One example is the amount of inflation compensation investors demand in the bond market. Over the next five years (the 5-year measure shown below), markets are pricing in inflation that is consistent with our expectations of some economic heat in the short-term as the economy reopens. Over the longer-term (the 5Y5Y series below, which corresponds to the five-year period that starts five years from now), investors for the moment are assuming inflation that is consistent with recent history as well as the Federal Reserve’s target.

Other data tell a similar story. The figure below shows a monthly composite measure that summarizes 22 different market- and survey-based measures of long-run inflation expectations, including market rates like those shown above as well as surveys of households and professional forecasters. This composite measure also suggests higher expectations, but the levels of these expectations remain well within historical levels.

The data in the figure are from CEA’s analysis based, in part, on Ahn and Fulton (2020), The Fed – Index of Common Inflation Expectations (federalreserve.gov).

Conclusions

We think the likeliest outlook over the next several months is for inflation to rise modestly due to the three temporary factors we discuss above, and to fade back to a lower pace thereafter as actual inflation begins to run more in line with longer-run expectations. Such a transitory rise in inflation would be consistent with some prior episodes in American history coming out of a pandemic or when the labor market has quickly shifted, such as demobilization from wars. We will, however, carefully monitor both actual price changes and inflation expectations for any signs of unexpected price pressures that might arise as America leaves the pandemic behind and enters the next economic expansion.